The objective of this SAFARI is to get us up-to-speed with what the 2021 trends and challenges are in the Market space. If you are a Credit Provider, an Accountable Institution or a Service Provider to these Industries you cannot miss the opportunity to be informed about the Macro Economics currently playing out and what the balance of 2021 might have in store for us. AfriGIS COO, Charl Fouche will be presenting on Tracking your Risks – mapping more than one risk and then superseding the maps.

AfriGIS presenting:

Tracking your Risks – mapping more than one risk and then superseding the maps

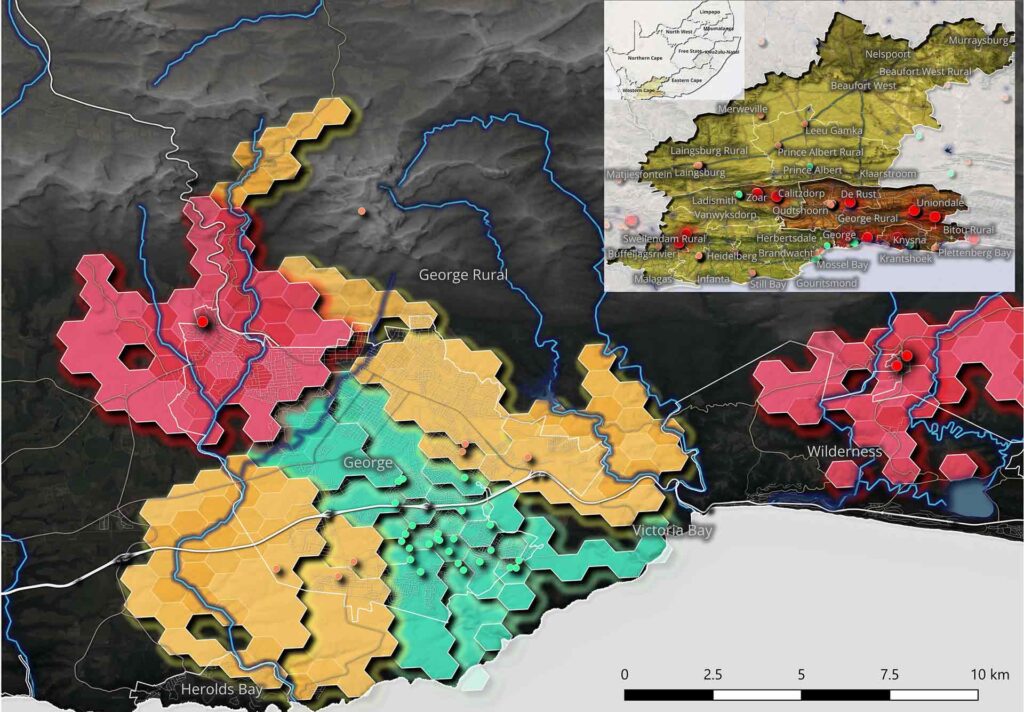

What rapid-response spatial intelligence knew before the Garden Route flooded again South Africa's Garden Route was hit by two cutoff low storms within a month, the second in early June 2026 bringing up to 200mm of rain across an already-satur…South Africa's Garden Route was hit by two cutoff low storms within a month, the second in early June 2026 bringing up to 200mm of rain across an already-saturated region with dams at full capacity, May's temporary road repairs still in place, and the N1 at Leeu Gamka eventually closing. Before that second storm peaked, AfriGIS had already used just four rapidly integrated spatial data layers roads, rivers, informal settlement locations, and storm warning data to identify 22 of the Garden Route's 209 informal settlements at extreme risk of losing all physical access, with Kannaland and George carrying 16 of those, enabling disaster management teams to pre-position resources and plan evacuation routes before conditions peaked. The deeper argument is that the same four-layer foundation becomes substantially more powerful with each additional dataset layered onto it: add deeds and cadastre data and an insurer can move to parcel-level flood underwriting; add CIPC business data and you can quantify revenue disruption, not just building damage; layer in infrastructure assets and Transnet, Sanral, and Eskom can each see where their balance-sheet exposure becomes critical. AfriGIS positions this building-block quality backed by 28 years of authoritative, never-crowdsourced verified data as the foundation for what national-scale spatial preparedness could deliver as SA's rainfall season runs through November.

Why static property data is costing South African short-term insurers their margins South Africa's short-term insurers are pricing property risk against municipal valuation rolls built for tax collection, updated on multi-year cycles, and reflecting a version of the country that no longer exists in many areas. As semigration accelerates to secondary hubs and infrastructure struggles to keep pace, a blocked stormwater drain or outdated flood wall can transform a historically low-risk property into an active hazard overnight. Insurers relying on lagging municipal records will miss these shifts entirely, and the exposure only becomes visible after a severe weather event. The solution is exact geocoding. By pinning property records to precise geographic coordinates, underwriters can overlay real-time spatial layers covering flood lines, fire hazards, weather patterns, and infrastructure constraints, enabling street-by-street risk pricing rather than broad municipal approximations. The same intelligence extends to operations: geofenced hail alerts warn policyholders before damage occurs, and satellite imagery cross-referenced with deeds data automates agricultural claims validation. Insurers who embed location intelligence into their workflows move from reactive loss management to proactive, precision underwriting.